- Home

- Blog

- Frontier Trading Desk

- Frontrunner - 27th March 2020

Frontrunner - 27th March 2020

COVID-19

- Frontier's message to customers

Frontier's number one priority will always be the health and safety of our colleagues, customers and those with whom we have contact during our normal business operations. We are actively and continuously monitoring the situation and basing our actions on the very latest advice from the Government. These actions currently include a range of measures such as minimising the number of people at our sites, colleagues working from home where possible, implementing social distancing measures and self-isolating when necessary. We have also implemented service contingency plans in order that we can continue to deliver a service which is 'business as usual', albeit with some changes to the way we operate. Read the full statement from Mark Aitchison, Frontier's Managing Director, here.

- Ensuring our customers and suppliers are paid promptly – digital payment

To ensure we comply with social distancing measures and that our customers and suppliers are still paid promptly, we have switched to a digital-only payment system. In our first statement about the current crisis, we made a commitment that 'our aim throughout this will be to deliver a full service and support...'. Part of that is ensuring that we continue to pay promptly our farmer customers for grain they have traded with us, and our suppliers for goods and services they have provided to us. If you are usually paid by cheque – we need your bank details. Click here to find out more.

- Ensuring we continue to share expert advice

One of our team's key roles is sharing expertise gained from our extensive trials and demonstration site network to help support their customers with business decision making. Whilst we have postponed all customer meetings, whether they be with groups or individuals, we are looking at a variety of ways to ensure that our customers can still benefit from our significant investment in trials work. These will include sharing expertise via, amongst other things, our blog, virtual plot tours and group video conferencing.

WHEAT

- Coronavirus drives wheat markets

The spreading of coronavirus and its impact on supply chains and foreign exchange has continued to be the primary driver for world wheat markets this week. UK prices have been particularly volatile, responding to wide swings in the value of sterling versus the euro. With sterling at its weakest, trading within a 5% range against the euro, 2020 London wheat futures rallied to new contract highs before losing value on Friday as sterling found renewed strength.

- Russia considers export restrictions

Internal flour prices reportedly reached record high levels in Russia this week with one trade group suggesting this would lead to flour shortages and warrant calls for limits to food exports. US wheat futures rallied to an eight-week high on concerns that Russia might restrict wheat exports. Russia is the world's largest wheat exporter and so far this season has shipped over 26 million tonnes of their 35million tonne target.

On Friday, the Ministry of Agriculture of the Russian Federation proposed setting up a quota for grain exports of seven million tonnes for the last quarter of the season (April, May and June), to protect their domestic supply amidst the coronavirus crisis. A similar situation was reported in the Ukraine, where concerns over coronavirus led millers and bakers to ask the Government to restrict grain product exports.

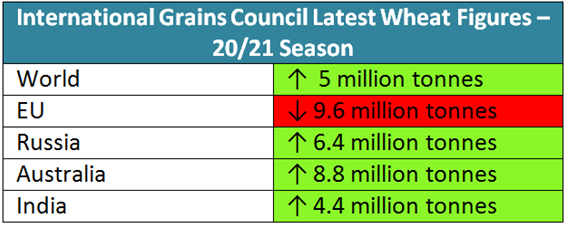

- Estimates see record 2020/21 world wheat production

It predicts gains for Russia of 6.4 million tonnes, Australia of 8.8 million tonnes and India of 4.4 million tonnes. However, a significant decline for the EU and overall production for the world's major wheat exporters is also anticipated. These values have dropped 9.6 million tonnes, bringing the current total to 380 million tonnes. World wheat stocks will rise 8.5 million tonnes to a record 283.2 million tonnes, but stocks for the major wheat exports will be 4 million tonnes lower, bringing these totals to 62.8 million tonnes. Prospects for Russia and Australia need to be monitored closely.

BARLEY

- Contrasting markets for old crop feed and malting barley

Demand for old crop malting barley has been decimated by the spread of Covid-19 and its consequential social distancing measures which are having a significant impact on beer sales in the service sector. As a result, any old crop malting barley that has not yet been marketed should now be considered feed barley going forward. At this stage, the timeframe for any recovery in demand is uncertain with the impact of the virus likely to extend into new crop.

Meanwhile, the UK has found export demand for feed barley over the last fortnight on the back of the significant fall in the value of sterling, particularly against the euro, which has given a late season boost to the UK export pace. The wider spread of the virus is putting a pressure on logistical infrastructure, but the UK is continuing to execute business both domestically and internationally. However, sterling is not the only currency that has faced recent pressures; the oil-based Russian rouble has also lost significant value, giving Russian exports a competitive edge on the global feed barley market.

- Spring fieldwork well underway throughout UK

The UK has experienced its best week of weather since the turn of the year, with lots of field activity from the south coast well into Scotland. A dry forecast into next week will allow for significant progress on drilling throughout the UK. France is also benefitting from the improved weather, and spring barley plantings have risen significantly from 40% complete last week to 72% complete this week. This is still far from the 97% completion rate this time last year. With the extreme volatility in the market at the moment, Frontier's feed and malting barley pools should be seriously considered as part of any marketing strategy. Please speak to your local Frontier farm trader to discuss further.

OILSEED RAPE

- Stable markets

In recent days, we have seen a remarkably stable spell for markets, with Brent crude trading close to $28 a barrel all week and sterling valued either side of 1.1 against the euro. French rapeseed futures have been confined to a narrow trading range, leaving UK physical prices virtually unchanged since last Friday. With new crop farm values above £300/t in most areas, it should be remembered that this achievement is largely down to the performance of the sterling which has devalued by 10% against the euro since the middle of last month. As a result, the cost of imports into the UK has risen by over £30/t.

- South American supplies tighten

A number of global factors have contributed towards more stabile markets. The influential Soybean and Corn Advisor, based in Illinois, put out an amended forecast for Brazilian soybean production, trimming one million tonnes from their previous estimate, which took their new estimate down to 122 million tonnes. Additionally, there has been talk of supply bottlenecks in Brazil and Argentina. The Brazilian real has been strong against the US dollar, eroding their price competitiveness. Elsewhere, firmer world energy prices have supported palm oil markets.

- Slow US soybean exports

In the US, there is still no sign of a surge in soybean exports to China. It is currently running 14% behind last year's pace and it looks unlikely that the 2019/20 total exports can match the latest forecast from the United States Department of Agriculture (USDA). However, with the bottom falling out of the ethanol market, there is bound to be a sharp reduction in DDG production in the US and this will give support to meal prices. It is difficult to predict how many US farmers might make a late switch in their planting intentions for harvest 2020 away from corn and into beans. Next Tuesday's USDA crop report could have given us some indication, but the survey work was done prior to the plunge in ethanol prices. It will be another three months until the next report in this series is published.

PULSES

- Marketing opportunities for new crop

Trading in old crop beans has almost finished with values edging a little lower due to lack of demand both in the UK and on the continent. Given the good drilling conditions for spring beans at this time, it is worth looking at marketing opportunities for new crop. Overall, there will likely be an increase in the bean planted acreage. Indications show that the winter acreage will be 40-50% lower than first intentions but, with an increase in spring area, it is likely that an overall increase of 10 -15% will be seen. Yield is going to be unpredictable with later plantings and some poorer than expected seedbeds, but overall we should expect a similar sized crop to last year.

- Strong values for new crop

New crop values are bearing up well with over £200/t available for feed bean movement pre-Christmas. In addition, we still have our successful bean pool open, as well as a premium bean buyback. Please contact your local Frontier farm trader for more details.

FERTILISER

- Nitrogen

This week the sun came out and drilling progressed at a great pace. Demand for fertiliser spiked, adding to an already full order book, meaning deliveries will be a challenge over the coming weeks.

The nitrogen market was already dealing with weaker sterling pushing import prices higher when the European market firmed in reaction to the closure of borders. European fertiliser co-ops and large distributors scrambled around the market, covering products to meet the likely demand in the next 3-5 months. Historically, most would have waited for the summer discounts, but with the borders likely to be closed for some time, they could not wait.

In the UK, CF Fertilisers is still producing Nitram, nitrogen sulphur grades and compounds at Ince and Nitram in Billingham. In France, a large ammonia plant was shut down due to staffing issues caused by Covid-19. Our suggestion would be to get orders in as soon as possible to allow the industry to get product on farm. Speak to your local Frontier contact for more information.

- Blenders

Issues with some raw material supplies along with a huge increase in demand is making spring 2020 a difficult one. The market has moved up £20-25/t this week due to a mixture of currency, European demand and shipping issues. More locally, we depend on staff at the blending plants to blend, pack and load fertiliser onto our trucks. The haulage industry is also facing problems, as much of the building and construction industry has gone into shut down leaving many hauliers with no back loads. Again, our suggestion is to book early to avoid delays in delivery.

Get in touch

Please speak to your local Frontier contact or email us at This email address is being protected from spambots. You need JavaScript enabled to view it. for more information or advice related to any of the topics and services mentioned in this report.

As a subscriber, you’ll receive email alerts each time a new blog is published so you can always stay updated with the latest advice and insights from our experts

Comments